Learn more about the people at Charity Bank

Our ESG principles and aims for net zero

Our careers for good and current vacancies

Our commitment to EDI

We’re entirely owned by charitable foundations, trusts and social purpose organisations.

About Us

Secured loans from £100,000 up to £500,000

Amplify your impact with a secured loan over £500,000+

Our Green Loans for developing a sustainable impact

Our expertise in development and construction projects

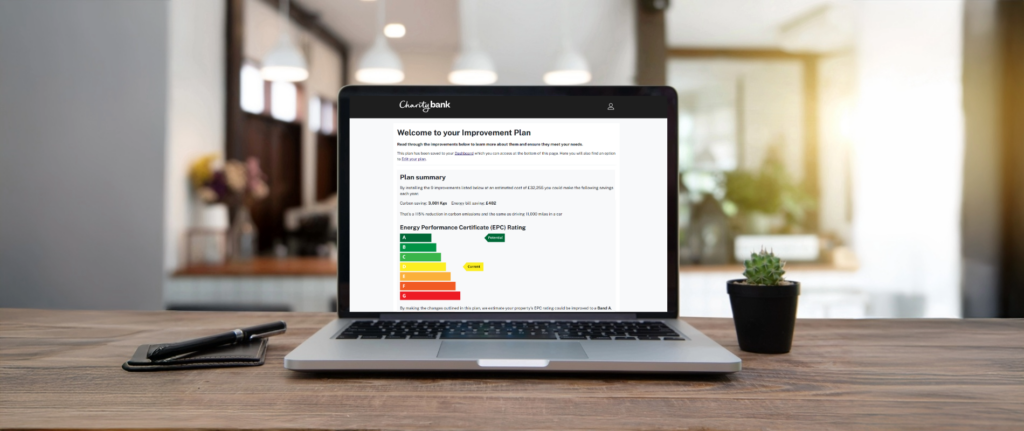

Our Energy Savings Tool can help social purpose housing providers plan energy-saving and sustainable property improvements.

Find out more

Personal Savings Accounts

Charities, Trusts & Clubs Savings Accounts

Business Savings Accounts

Credit Union Savings Accounts

In a Charity Bank ethical savings account, your money is a powerful force for good.

Our Savings Accounts

The latest news and resources from Charity Bank.